Capital Optionality in Uncertain Markets: When to Raise, When to Wait, and When to Self-Fund

News, insights and updates from the team at Bloom Equity Partners

Happy Friday technology investors, operators, and enthusiasts.

We’re here again with The Bi-Weekly Bloom – one of the best resources for Private Equity, Enterprise Software, and Technology news. In each edition, we delve into:

PE Interest in Technology

Our team’s favorite articles and podcasts from last week

Insightful tweets from fellow investors and operators

Join nearly 10,000 readers for a summary of our favorite software insights, articles, podcasts, tweets, and news headlines, subscribe below:

Capital Optionality in Uncertain Markets: When to Raise, When to Wait, and When to Self-Fund

Capital remains available, and credit markets are functioning. However, underwriting is more disciplined, covenants are tighter, and performance expectations are clearer than in prior cycles.

The environment may not have closed, but it has certainly sharpened. That shift makes capital optionality a central strategic question for boards and founders. Capital optionality is not merely access to funding. It is the ability to evaluate, with discipline, whether raising capital advances durable outcomes or simply changes the company’s risk profile.

Having Options vs. Exercising Options

This distinction is the conceptual core of the decision. Having options means that capital providers are willing to transact. Exercising options means accepting the governance structure, ownership implications, and performance expectations embedded in that capital.

Confusing the two has real costs. Boards often equate market interest with validation, yet the existence of capital does not obligate its use. Exercising an option alters control, strategic pacing, and future flexibility in ways that compound over time.

A disciplined board evaluates whether capital accelerates a durable strategy or merely extends runway under tighter oversight.

Boards typically exercise capital optionality in three ways: majority investment, minority growth capital, or continued self-funded growth.

Path 1: Majority Private Equity Investment

A majority PE investment is a structural shift. It introduces formal governance, defined reporting rhythms, and a shared exit horizon. Capital is paired with institutional discipline.

This path is most appropriate when the growth opportunity is time-sensitive and capital-intensive. If market leadership requires rapid geographic expansion, significant M&A, or meaningful product investment, majority capital can compress timelines and professionalize execution. But it transfers operational control, it embeds a defined liquidity expectation, and it changes the strategic cadence from open-ended to milestone-driven.

This path works when founders are genuinely aligned with a shared exit timeline and governance structure, not merely willing to tolerate one. If the founder’s horizon or risk appetite diverges, friction will surface later.

Path 2: Minority Growth Capital

Minority capital appears less intrusive. It preserves day-to-day autonomy while injecting fuel for expansion. Governance rights may be lighter, and control is formally retained. Yet, minority capital defers the control conversation.

Performance expectations are embedded in the structure. If growth targets are not met, future financing rounds can shift leverage. Founders who take minority capital without acknowledging this dynamic often find themselves more constrained at the next inflection point than they anticipated.

Minority capital is effective when expansion requires funding, but the company retains strong internal control of its growth levers. It is less effective when capital is used to compensate for structural inefficiencies that will resurface under investor scrutiny.

In structures like this, even minority rounds embed return thresholds that can shift control dynamics over time if performance deviates from the plan.

Path 3: Self-Funded or Organic Growth

Self-funded growth maximizes control, limits dilution, and preserves cultural continuity. It removes external governance pressure and exit timelines. It makes sense when the growth plan does not require external capital to succeed and when the value of control preservation exceeds the incremental benefit of outside funding. Companies with strong sales efficiency, positive cash conversion, and manageable capital intensity often fit this profile.

The constraint is competitive response speed. In markets that reward rapid scale or aggressive consolidation, a self-funded company may move more slowly than a capitalized competitor. Boards must evaluate whether pacing risk outweighs dilution and governance tradeoffs.

The Core Variables Boards Must Weigh

There is no universal sequence for evaluating capital decisions. The relative weight of each factor depends on context. What matters is understanding how they interact.

Capital Intensity of the Growth Plan

If the strategy requires heavy upfront investment in product, infrastructure, or acquisition, external capital may compress execution risk. If growth is incremental and internally financed, outside capital may be unnecessary.

Sales Efficiency and Cash Conversion

Strong unit economics reduce reliance on external funding. Weak efficiency increases vulnerability to investor expectations. A company with rapid payback periods and predictable cash flow has more optionality than one reliant on sustained burn.

Competitive Pressure

Markets characterized by rapid consolidation or platform dominance often reward speed. In slower-moving or fragmented markets, disciplined organic growth may outperform capital-fueled expansion.

Risk Tolerance

Capital introduces governance oversight and performance milestones. Leadership must assess whether they prefer shared accountability with acceleration or independent pacing with concentrated risk.

Long-Term Ownership Goals

Exit horizons and legacy objectives matter. A founder seeking liquidity within a defined timeframe may rationally pursue majority capital. A founder prioritizing long-term stewardship may find the cost of external control too high.

A capital-intensive plan in a competitive market may justify dilution if sales efficiency is proven and leadership is aligned on exit timing. Conversely, a capital-light business with strong cash flow and long-term ownership goals may rationally avoid external funding even if investors are interested.

Capital optionality means evaluating these interactions deliberately rather than defaulting to whichever option is currently accessible.

Capital Optionality in Practice

Consider a software company generating $10 million in ARR, growing at 25% annually. The company raises $30 million from a growth investor at a $120 million pre-money valuation, implying a $150 million post-money valuation and a 12x revenue multiple. The investor acquires 20% ownership and underwrites to a 3x return over five years, implying a target exit valuation of approximately $450 million.

To support that outcome, the company must sustain or accelerate growth while expanding margins. If growth slows or efficiency declines, the required exit multiple increases or additional capital may be needed, introducing further dilution.

If the company raises a second round two years later at a lower multiple, early dilution compounds. A 20% initial stake can expand meaningfully depending on structure, liquidation preferences, and performance shortfalls. The decision to raise capital established a performance threshold, a return expectation, and a future ownership trajectory.

This is the practical expression of capital optionality. The question is not whether capital is available but what the company commits to deliver when it accepts it.

Conclusion: Choosing Capital With Discipline

Capital decisions shape governance, risk profile, and long-term outcomes in ways that compound over time. Raising capital is neither inherently aggressive nor conservative. Waiting or self-funding is not necessarily risk-averse. It may reflect the most disciplined assessment of growth requirements and control preservation.

The strongest companies treat capital as a strategic instrument, not a milestone. The discipline isn’t in keeping all paths open but in knowing which one to close. Boards that make that choice deliberately, against a clear set of criteria, will consistently outperform those that raise because the option was available.

For continued analysis on private capital dynamics, strategic positioning, and decision frameworks for operators and investors, subscribe to future updates from Bloom Equity Partners.

About Bloom Equity Partners

We’re big fans of mission-critical enterprise software, technology and tech-enabled business service companies with a competitive moat and a loyal, diversified, and growing customer base.

Whether the business is bootstrapped, VC-backed, or a division of a larger organization, Bloom is completely agnostic to the structure. We are actively seeking investment opportunities that fall within the criteria below. We welcome the opportunity to discuss potential investments with founders, operating executives and intermediaries.

Our Investment Criteria

Industry: B2B Software and Technology-Enabled Companies

Geography: North America, Europe, Australia and New Zealand

Revenue: $5M - $50M

Growth: No requirement

Profitability: Negative - $10M EBITDA

Investment Type: Operational control required

If you or someone you know is considering selling or investing in their business, we would love to learn more! Check out our referral partner program, which compensates referrers for introductions that lead to affirmative outcomes. Reach out to: Abe Borden, Principal – abe@bloomequitypartners.com

What We’re Reading and Listening To…

Podcast: How to Scale Without Burning Cash with Manu Diwakar, Chief Financial Officer, Virta Health

Podcast: Strategic Planning for Fundraising Success

Article: 6 Key Lessons on Bootstrapping vs Fundraising for Founders

Article: Startup bootstrapping: Understanding the pros and cons

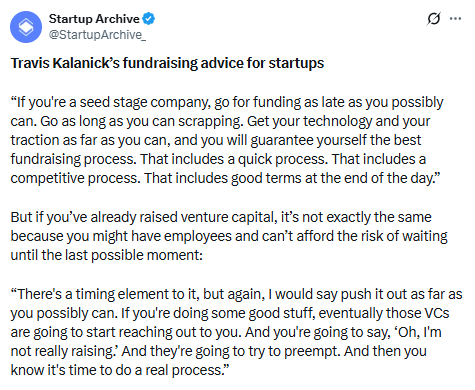

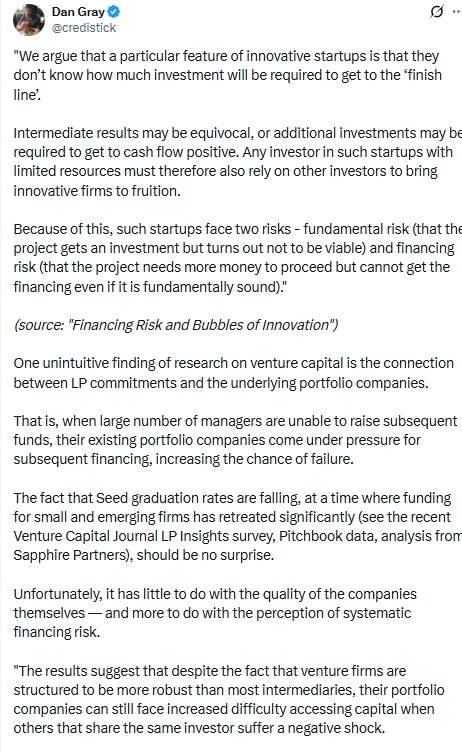

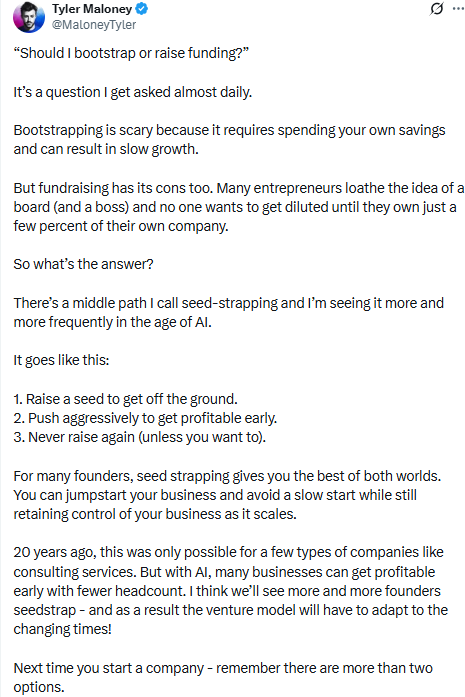

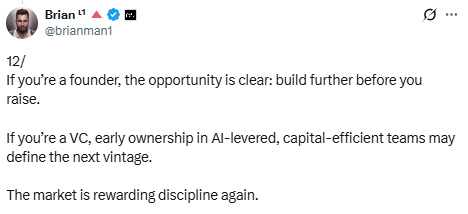

Favorites from the Ecosystem

Investors…

Operators…

Founders…

If you’re enjoying The Bi-Weekly Bloom, we’d appreciate it if you shared it with your network.