Wrapping up 2023

News, insights and updates from the team at Bloom Equity Partners

Happy Friday technology investors, operators, and enthusiasts.

We’re here again with The Bi-Weekly Bloom – one of the best resources for Private Equity, Enterprise Software, and Technology news. In each edition we delve into:

PE Interest in Technology

Our team’s favorite articles and podcasts from last week

Insightful tweets from fellow investors and operators

Join over 8,500 readers for a summary of our favorite software insights, articles, podcasts, tweets, and news headlines, subscribe below:

Wrapping up 2023

As 2023 ends, we wanted to recap some of the highlights The Bi-Weekly Bloom shared throughout the year in Private Equity, Enterprise Software, and Technology news.

Private Equity and Technology

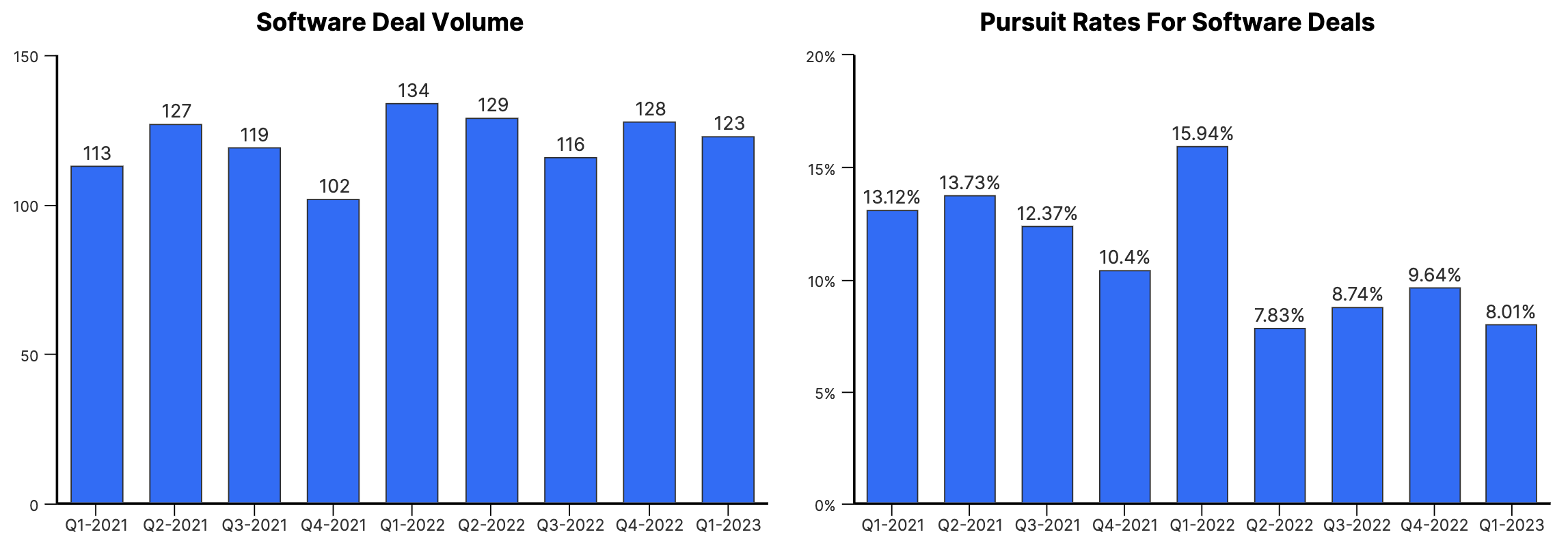

Software M&A Outlook in 2 Charts

We noted several insights from Axial’s 2023 Software M&A Market Outlook:

Cybersecurity, HealthTech, FinTech, Artificial Intelligence, and GovTech were the most appealing sub-sectors for M&A interest in 2023

Diminishing access to capital offered buyers more attractive opportunities than in recent years.

“Tech” in Private Portfolios is Mostly Software — A Sign of Resiliency

According to a Bain PE Report issued in February 2023, 88% of the technology investments in buyout funds are software companies, significantly less volatile than public tech companies.

Private Equity’s Interest in Technology Continues to be Strong

With record dry powder, the adaptation of complex portfolio strategies that leverage relationships and expertise, lower stock prices and increased regulatory scrutiny for public funds, private equity is starting to gain an edge against corporate buyers. Private equity buyers led seven of the ten most extensive IT M&A deals in 2022.

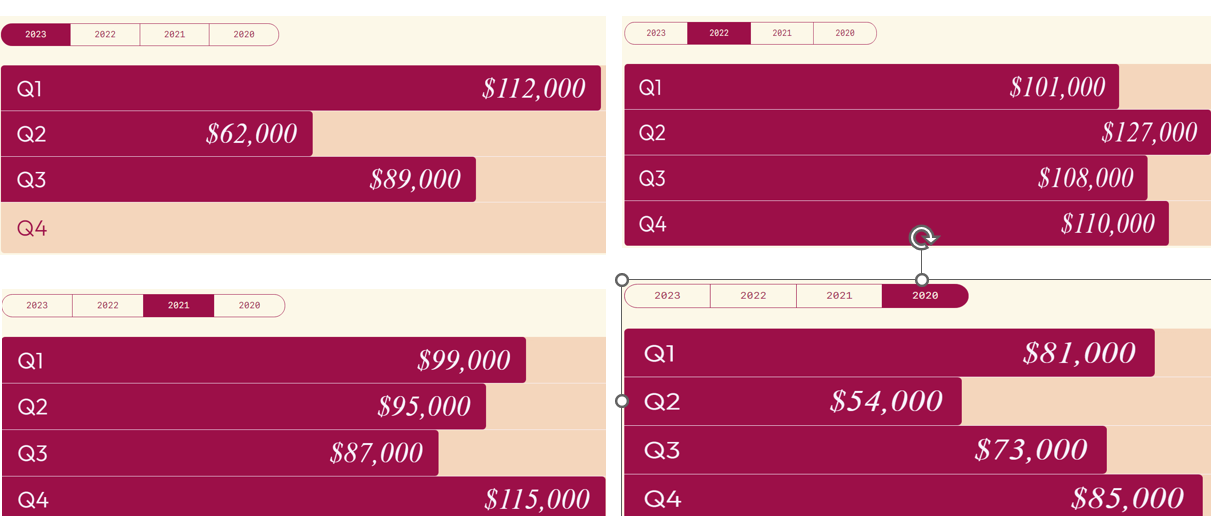

The Current Tech M&A Landscape

We gleaned some critical insights from Tech M&A Q3 2023 report by CBI Insights,

Global tech M&A deal volume dropped to its lowest point since early in the pandemic in Q3 2023.

Financial Deals Remain Steady. Due to macroeconomic uncertainties and a lack of high-quality assets, financial sponsors tread carefully. Most financial deals were private company buyouts.

Smaller companies with fewer than 100 employees see more deals

SaaS Market

SaaS M&A: Opportunities Abound

According to the Software Equity Group (SEG) 2023 Q3 SaaS M&A Report, investors are still buying SaaS companies despite a challenging market. Other insights included:

Deal volume continues rising. Based on data from previous quarters, all indications point to the SaaS industry achieving a record-breaking year in 2023. Increases in SaaS M&A activity have proven to be more than a pandemic-driven trend, with more businesses globally turning towards cloud-based, modern technology.

Private equity appetite for SaaS M&A represented most SaaS deals in 3Q23. PE-backed strategics have continued to seize the opportunity presented by record levels of dry powder and strategic synergies, representing 50% of all deals.

SaaS Trends Report: Prices Rising

Despite the challenging economy, businesses still buy and renew SaaS software — it’s just taking longer, costing more and under more buyer scrutiny, according to Vendr’s “The SaaS Trends Report” for Q3 2023. Other pricing insights include:

ACV climbs 43% quarter-over-quarter but remains lower than the three-year average.

Sellers raise prices to maintain ACV levels as buyers prioritize efficiency by scrutinizing line items and cutting seats.

Acquiring customers costs more (CAC reaches a three-year high in Q3 2023). Net new purchases are down 37% YoY as SaaS buyers focus on receiving the best possible renewal deals rather than buying new software.

2023 SaaS Benchmarks: What Sets Top Performers Apart

We gleaned some crucial details from the Capchase 2023 SaaS Benchmark Report to demonstrate what it takes for top SaaS companies to stand apart from the competition.

The healthiest businesses are growing three times faster than the average despite maintaining higher Net Margins.

Companies with the most robust Rule of 40 (ARR Growth + Net Margin) will likely achieve profitability sooner.

Top performers focus on efficiently acquiring new logos rather than customer retention.

These businesses keep Customer Acquisition Costs (CAC) low and recoup costs in half the time of their peers.

Trends in SaaS Sales Performance

We reviewed Capchase’s B2B SaaS Sales Cycles in 2023: New Insights and Data, which tracks the B2B SaaS industry’s sales performance in today’s economic environment for insights including:

Sales cycles are 27 days longer in the first half of 2023 than in 2022 due to increased negotiations and more stakeholders involved in purchasing.

ACV cooling compared to previous years.

Rigid payment terms prevent sales from closing quickly.

Today’s SaaS Landscape: Efficient Growth

In today’s challenging economic climate, SaaS leaders face a difficult decision: improving growth or efficiency. Results from the ICONIQ report, The New Era of Efficient Growth: Topline Growth and Operational Efficiency, recommended efficient growth.

As growth has slowed, companies have focused on reducing spending and extending the runway via levers such as hiring freezes, reductions in force (RIFs), tool rationalization, and performance management. Sales efficiency declined as selling SaaS tools and platforms has become more challenging in the macro environment.

ICONIQ identified five key metrics highly representative of a B2B SaaS company’s overall growth and efficiency.

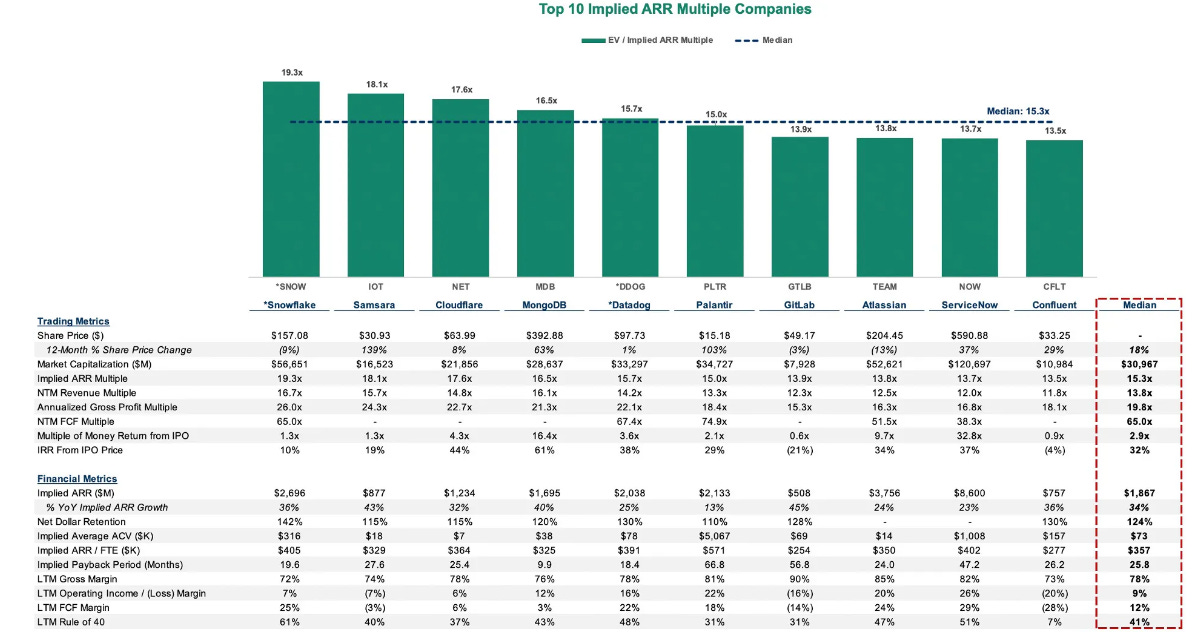

State of Public SaaS Industry

While we typically focus on the Private Equity space, we thought this report on the public SaaS market would be fascinating to our readers as public market data provides context not readily available in the private markets. The update from Meritech offered charts and results in the public market SaaS market, including:

Trended Valuation Multiples

Operating Metrics and KPIs

Growth and Profitability Analysis and Regressions

Company Rankings

On to 2024

What will 2024 bring? Whatever happens, The Bi-Weekly Bloom will keep you informed with all the essential Private Equity, Enterprise Software, and Technology news. Stay tuned!

About Bloom Equity Partners

We’re big fans of mission-critical enterprise software, technology and tech-enabled business service companies with a competitive moat and a loyal, diversified, and growing customer base. Whether the business is bootstrapped, VC-backed, or a division of a larger organization, Bloom is completely agnostic to the structure. We are actively seeking investment opportunities that fall within the criteria below. We welcome the opportunity to discuss potential investments with founders, operating executives and intermediaries.

Our Investment Criteria

Industry: Enterprise Software, Technology and Tech-Enabled Business Services

Geography: North America, Europe, Australia and New Zealand

Revenue: $5M - $50M (>70% recurring)

Growth: 5%+ annual revenue growth

Retention: >80% gross annual customer retention

Profitability: Positive EBITDA or near breakeven within twelve months

Investment Type: Operational control required

If you or someone you know is considering selling or investing in their business, we would love to learn more! We just launched our referral partner program, which compensates referrers for introductions that lead to affirmative outcomes.

What We’re Reading and Listening To…

24 Predictions for SaaS in 2024

The Future of Business Software

Unfolding the Future: 2024 Fintech Trends

Favorites from the Ecosystem

Investors…

Operators…

Founders…

If you’re enjoying The Bi-Weekly Bloom, we’d appreciate it if you shared it with your network.